Walls between channel-specific and traditional retail marketing roles are beginning to crumble, according to new data outlined in Forrester Research’s “Commerce Technology And Platform Investment Trends – 2013” report.

Walls between channel-specific and traditional retail marketing roles are beginning to crumble, according to new data outlined in Forrester Research’s “Commerce Technology And Platform Investment Trends – 2013” report.

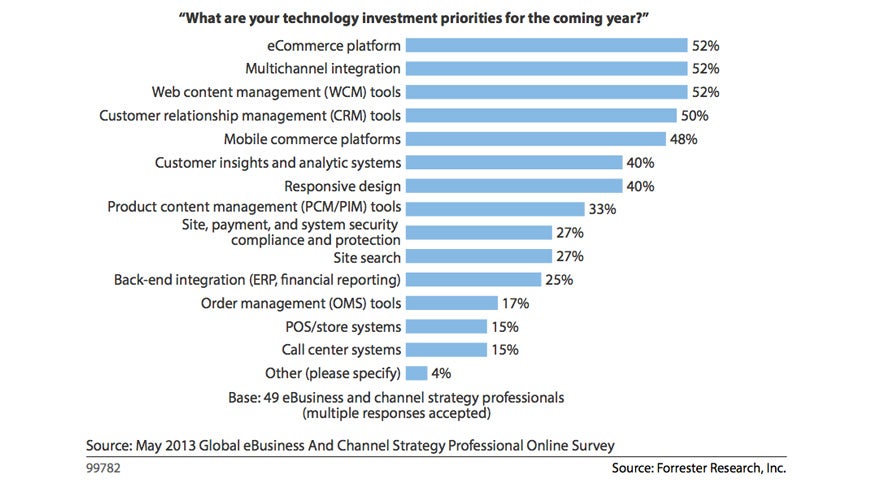

With online retail spend in the US forecasted to grow 9.9% between 2012 and 2017 and digital channels (online, mobile and tablet) estimated to account for 10% of retail sales, or $319 billion in the US alone by 2015, more brands are expected to appropriate funds toward digital innovation. Additionally, commerce technology investments are top of mind. According to the survey, 62% of retailers said omnichannel integrations were their top priority in the coming year.

Peter Sheldon, principal analyst and lead author of the report, spoke with AdExchanger.

AdExchanger: Where are companies investing the most with omnichannel?

Peter Sheldon: The first thing is, we used to talk about e-commerce as a channel and I think that if we go back two to five years ago, it really was a standalone channel and there was a director of e-commerce who had P&L responsibility for online sales. There have certainly been investments in that channel over the last decade, but that investment has seen significant increases over the last five years as we’ve seen growth in the online channel. Then there’s the other channel, which is the store’s channel, so the head of stores who also has a P&L. We’ve seen these two groups come together. In some companies, they’re actually merging the groups together and stopping talk about channels all together.

This is causing an uptick in terms of investment in commerce technologies, because they’re not just investing in the online channel, but now in mobile, tablet, in-store experiences, mobile POS in store, execution of omnichannel initiatives like ship from store, pickup in store, and so the increase of investment in commerce technologies is rising. I’ve done a number of consulting projects with clients this year who are effectively looking to validate the business case for doubling their investment in commerce technologies. There is lots of money being poured in to the technology piece.

These changes are impacting marketer decisions as well. How does this impact them on a role basis?

We see this multichannel integration piece, which isn’t really a surprise but this is sort of top of mind for retailers at this moment. They’re spending money and investing … in ship to store, store to store, ship from store.

They have content management on there as well, and you see e-tailers and others struggling with content-management capabilities as corporate marketing and e-commerce marketing teams kind of come together and play a much tighter role together. In some cases, they operate almost as a single team and all of a sudden, there’s a lot more priority of how we manage content and this no longer content for just the online commerce site. This is print media content, ad content, print content in stores. This is all being managed more now in a cohesive manner so there’s certainly investment in content-management systems.

Has there been a “democratization” of media and content?

I think what we’ve seen in the past is a corporate brand and then maybe an e-commerce marketing department were sort of siloed divisions. We’ve seen democratization because now what’s driving this is increasingly the content was originally [designed] for the Web. If we think about product content, translated content, banners, offers – these things used to be exclusive to the Web channel and now they’re being used on Web, mobile, tablet. Even print guys are putting [online] product reviews and ratings all over their print content.

It’s almost a natural progression where we’re no longer doing marketing in channel siloes. Anyone involved in marketing initiatives now are becoming omnichannel in nature. We’re starting to see chief omnichannel officers. We’ve now got this challenge where different groups need to collaborate around content initiatives.

With players like eBay launching cohesive enterprise marketing solutions and more traditional brick-and-mortars playing around with flexibility in fulfillment, is eBay more of a competitor or an ally to a traditional retail brand?

EBay made some acquisitions in the space of commerce technologies, like GSI Commerce, Magento and others over the last few years and they’ve sort of consolidated those acquisitions into eBay Enterprise. If you think about it, it actually makes a lot of sense. They have PayPal and [the] eBay marketplace and now eBay Enterprise. Increasingly, eBay now has some pretty deep capabilities in terms of [servicing] their enterprise clients.

We’re primarily talking about retailers and branded manufacturers here. With their execution in omnichannel strategies, commerce technology and so forth, and eBay kind of formalizing these capabilities and saying, ‘We now have a fairly large set of services and technology to bring to the table’ from fulfillment with GSI to … a lot of the stuff they’re doing in-store like their kiosks with Kate Spade, the e-commerce capabilities with Magento and the broad suite of marketing and services programs. None of this is new. They’ve sort of had all this since the acquisition of GSI, but this is sort of a formal recognition and a stake in the ground of their rebranding to say eBay is not just a consumer-to-consumer company. They are now going in to retailers and saying, ‘We can help you with your strategy.’

Are these shifting commerce investments changing relationships behind closed doors?

Absolutely. Five to seven years ago, e-commerce projects were done within the IT groups. They were bought by the CIO. Then, we saw this shift where as retailers and brands sort of built up their own e-commerce team, there was then a VP of e-commerce hired to help P&L … with the online channel. So we saw a big shift over the last two years where these types of commerce technology decisions were being led by the VP of commerce rather than by IT.

What we’re seeing today is as these e-commerce technology decisions become far more strategic to the organization as they are empowering mobile, tablet and in-store experiences, not just online because there are more digital touch points. These are strategic decisions. The decision [made now about] commerce technology platforms, I would say, is more strategic than any of their other software replatforming initiatives.

It still has the attention of the CEO, the board of directors if they’re a publicly traded firm. Once they get down to the final [stages] … a vendor will have to be approved by not only the CEO and COO, but owners of the company. This is the shift we’re seeing now. This technology impacts marketing and store operations. These decisions are not being made in isolation anymore.