As programmatic buying in China continues to pique marketers’ interest, demand-side platforms working in the country are growing in revenue and importance.

As programmatic buying in China continues to pique marketers’ interest, demand-side platforms working in the country are growing in revenue and importance.

Internet market research firm iResearch recently released an excerpt of its China DSP Market Trends Report 2013, including the market size of DSP display advertising in China, or the amount of ad spend that is initiated via DSPs.

In 2012, DSP ad spending was 550 million Yuan (or approximately $90.2 million*), which iResearch forecasts will grow 179.5% in 2013 to 1.53 billion Yuan ($251 million). By 2017, the market is expected to reach 17.2 billion Yuan ($2.82 billion).

“We are surprised that the DSP market in China last year was still quite small, but it has a very impressive growth rate,” said Will Tao, Analysis Director at iResearch, in an email to AdExchanger. “Many companies have set up their DSPs and have proven that it is valuable. The market is in its introductory stage and is beginning to grow rapidly.”

The report also looked at the vendors in the DSP space, including AdChina, iPinYou, MediaV, Yoyi and others, analyzing their abilities in four areas: product offering and media source, data capabilities, product function, and service capacity and technology investment.

“DSPs are the future of advertising, especially to display ads,” Tao said. “In China, the growth rate of display ads is flattening. Hence, DSPs could bring new opportunities to the advertising market. With DSPs, we are able to improve ad sales efficiency and attract more advertisers.”

The report noted that DSPs in China take on many roles in the industry chain, something that is unique compared to the programmatic buying space in other countries. One example is how DSPs in China must offer more data capabilities, because many publishers and advertisers are slow to share their data due to privacy concerns.

“The quality and quantity of data are very important to the results of DSP ads,” Tao added. “It is the base of all deployment strategies and algorithm optimization. However, data is quite hard to find in China due to lack of data integration and analysis in China. DSPs have to collect data by themselves.”

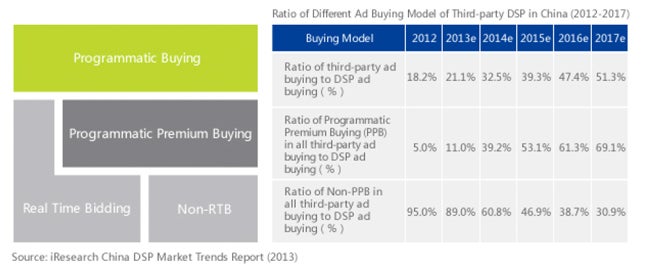

Currently, within the newer programmatic space in China, real-time bidding plays the largest role. But portals and publishers, which hold a lot of power in the space, are encouraging more use of premium programmatic buying—and iResearch’s data shows how much this will grow in the coming years.

By 2017, iResearch forecasts that more than 50% of programmatic ad placements through DSPs will come through third-party ad buying, as opposed to private DSPs owned by larger advertising agencies. And while real-time bidding will grow in China, premium programmatic buying will eventually overshadow it, as publishers continue to keep premium ad placements, such as homepage ad buys, away from RTB.

According to iResearch, premium programmatic buying will account for 11% of third-party DSP ad buys in 2013, rising to 69.1% in 2017. Conversely, the ratio of non-premium programmatic buying, or RTB, will shrink in the coming years. In 2012, the non-premium programmatic buys accounted for 95% of third-party ad buys, which will drop to 30.9% by 2017.

* Calculations done using XE.com, as of Nov. 12, 2013.