Yahoo has reported it’s Q1 2013 results. Get the release here. And, the earnings call slides (PDF).

Yahoo has reported it’s Q1 2013 results. Get the release here. And, the earnings call slides (PDF).

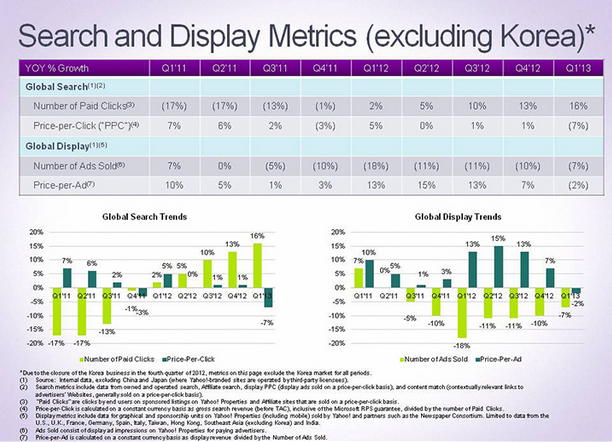

Display “Highlights” from the release:

- GAAP display revenue was $455 million for the first quarter of 2013, an 11 percent decrease compared to $511 million for the first quarter of 2012.

- Display revenue ex-TAC was $402 million for the first quarter of 2013, an 11% decrease compared to $454 million for the first quarter of 2012.

- The Number of Ads Sold (excluding Korea) decreased approximately 7% compared to the first quarter of 2012.

- Price-per-Ad (excluding Korea) decreased approximately 2% compared to the first quarter of 2012.

Prior to the earnings release, JP Morgan analyst Doug Anmuth was “forecasting total 1Q net revenue of $1.11B (+3.2%), EBITDA of $362M, and EPS of $0.27, essentially in-line with consensus.”

Reading the tea leaves of today’s earnings release, if you go by GAAP standards, looks like Anmuth was right. Yahoo says in the release: “GAAP revenue was $1,140 million for the first quarter of 2013, a 7% decrease from the first quarter of 2012. Revenue excluding traffic acquisition costs (‘revenue ex-TAC’ [or ex Traffic Acquisition Costs]) was $1,074 million for the first quarter of 2013, flat compared to the first quarter of 2012.”

Also earlier in the day (this is me stalling before the earnings call), Pivotal analyst Brian Wieser struck a foreboding tone for Yahoos and their publishing competitors: “While total online advertising posted a solid growth rate of 15% during 2012, we can clearly see that if we strip out growth from Google and Facebook, the rest of online advertising likely grew by 3.8%. This bodes poorly for conventional web publishers such as Yahoo, as Google and Facebook are likely to remain as the most dominant sellers of online advertising.” The last thing Mayer will want Yahoo to be in 5 to 7 years is a conventional web publisher. This is a b-school case study of the future with Mayer teaching class – will it be a “learning experience” or triumphant achievement? We’ll see.

The Yahoo earnings call music is big and brassy. It’s all about tone, isn’t it? 5p ET is almost here.

If you’re refreshing this page on AdExchanger – why wouldn’t you? – you can listen to the live call here.

Another highlight from the release is Yahoo’s new partnership with Google: “The Company announced a global, non-exclusive agreement with Google to sell display ads on various Yahoo! Properties and certain co-branded sites using Google’s AdSense for Content and AdMob services. By adding Google to its list of world-class contextual ad partners, Yahoo! can serve users with ads that are even more meaningful and personal.” From here, expect more Google ad tech flowing through the Yahoo pipes as Mayer shifts the Yahoo strategy to mobile. The former Googler lives what she knows – and Google ad tech is by and large better than Yahoo’s. (understatement)

Pre-call observation: The expectations bar for this earnings call are so low that even hearing Mayer’s voice will be a good thing.

Pre-call observation: By the way, as we wait, I’d like to talk about that $30 million-plus Q1 Summ.ly acquisition. Did Yahoo overpay for a two or three person company? Sure. But does Yahoo need to let young entrepreneurs know that they can make big bucks making cool mobile products for Yahoo? Yes. That was a $30 million press release to the Valley.

Pre-call observation: They changed the earnings call music to something more pensive, brooding – mono, not stereo. IR must have been reading AdExchanger and objected to my characterization of the music earlier. Yahoo IR: “We must let Wall Street and AdExchanger know we are controlling costs. Somberize the music.”

Pre-call observation: There’s a sense by some that agencies may be buying around Yahoo. Could be, but not if they’re an agency trading desk. They’re drinking up that sweet Yahoo inventory in Right Media Exchange as much as they can – brand safe, high performing, scale, standard IAB ads – “more please.”

The call has begun!

CEO Marissa Mayer takes the reins of the call from Yahoo IR. She’s pleased with execution in spite of flat results and says that this transformation will take years (see above). She wants Yahoo to build beautiful products in their “initial sprint.” “Sprint” is such a product person word.

She says Q1 resumes tripled in terms of hiring. But what she didn’t say is what they put behind their new recruitment efforts.

14% of new hires are “boomerangs” (her word) – they came back to Yahoo in Q1.

Scott Burke gets a shout out as the leader of ad tech and in charge of new monetization products. Is former Aol-er Ned Brody far behind?

Finally, Mayer discusses a couple of new Yahoo acquisitions and says new products are coming.

Web stats show growth in spite of display’s slump… she didn’t link the display part on the call.

Summly, Google and Dropbox are given shoutouts and she says product progress is “so very early.” Very very.

Yahoo keeps buying hundreds of millions of dollars worth of its own shares. This will come in handy when they start doling out more options to big name hires and acquisitions.

Finance takes over the call – see the release. Search, and “click yield” improvements.

Display suffered from slower traffic, says Finance. Huh, that seems to contradict what I heard earlier in the call. Stats showed traffic growth. Oh well.

The company made about $200 million depending on your favorite accounting practices. Slide for you (all slides here – PDF)…

Finance says that the introduction of a scarcity strategy last year is having a positive effect on yield in spite of sliding revenues. We’ll see,but it can’t hurt.

Lots of financial info that I’m not covering at this point in the call – I’ll be curious what Wall Street says. Expectations sound flat for future quarters. From here, Alibaba, Yahoo Japan are the (eventual) cash to be used for acquisitions of the future.

CEO Mayer takes back the reins from Finance and starts talking about “sprints” again leading to a “chain reaction.” User growth, higher engagement, and, ultimately, more revenue. Gotta build first.

Three hundred million mobile daily users for big Y. Personalization will be key for content and advertising at Yahoo… She did not say “native ads” but it felt like she wanted to.

Mayer emphasizes partners again, including Google, Facebook, Apple and Microsoft. Here’s the good news in display: The pace of decline in the number of ads sold is decelerating.

Wall Street Questions

Heath Terry from Goldman Sachs asks about decline in ads sold — was it about scarcity or the move to mobile, or? Mayer says traffic trends are declining but not as fast. More ads are being sold. Pricing is the thing, says Mayer, as apparently mobile is impacting revenue negatively. This is a familiar refrain in mobile markets.

Click volume – partners are being brought in. (To click?) The search deal with Microsoft continues to be a big question for Wall Street about Yahoo’s future revenues.

Display revenues ex-Traffic Acquisition Costs (TAC) – when will they turn around, wonders Wall Street? Mayer is clear that she and her team are focused on making good products but that some turnaround for display will happen in the second half of this year. Hard to know if that means it will be flat, a slowing of the display decrease, or what.

RBC’s Mark Mahaney asks if Google can get more involved with Yahoo, considering regulatory issues. Mayer says that current partnerships is all she is willing to discuss but is willing to “explore new opportunities.” Mahaney followed up regarding acqui-hires vs. in-house talent to carry out a mobile strategy and what will be needed. Mayer said it will be a mix basically.

Ben Schachter of Macquarie wants to know if user improvements can drive search share. Wall Street is hard to please. I believe Google owns Search. Mayer still says she wants to maintain and then grow share. If she has a sticky product, that could happen. But it isn’t today.

Yahoo sales team re-organization (again) – Wall Street wonders what the impact will be as Henrique De Castro and Marissa Mayer swing their axe in Sales. Yahoo will be targeting industry verticals rather than having, say, a display seller sell across all verticals.

More “beating of dead horse” on the growth of user engagement and pricing challenges of ads sold. Mayer says mail display ads started getting more clicks after a user interface change, but pricing didn’t change until after analysis of user results.

“Programmatic buying” makes the call courtesy of a Wall Street analyst. Is it impacting Yahoo negatively? The answer is according to Mayer: “We do have a healthy programmatic buying business. That said, we should be doing more in the programmatic space.” But, she stressed that a healthy mix needs to happen between “premium” (direct sold) and non-guaranteed inventory.

Jefferies Brian Pitz goes right at programmatic and whether Yahoo has the tools or ad tech. Mayer gives a short, politically-correct answer and stresses that she wants to be competitive and best-of-breed. As for Right Media Exchange, she says “We’re in the top two or three globally.” My reaction: she’s not enthused about investing in ad tech. It is not a priority. She will use partners – “Google here we come!”

More search talk, a bit more on mobile and the less than attractive pricing Yahoo is seeing. She thinks its a question of user pricing and formats for advertisers among other attributes.

This call is over one hour long. She seems to be taking all questions.

The Yahoo Toolbar – is it done for? Now, there’s a question. I haven’t thought about it lately. Mayer said more distribution is always of interest.

Mayer offers “her summarizing thoughts” and says the Summly technology that Yahoo recently acquired had compressed her 2,000 word script to 140 characters. Hmmm.

And the call is over!

If you want to read the transcript, visit Seeking Alpha here.