“Data-Driven Thinking” is written by members of the media community and contains fresh ideas on the digital revolution in media.

“Data-Driven Thinking” is written by members of the media community and contains fresh ideas on the digital revolution in media.

Today’s column is written by Tom Triscari, CEO of Labmatik.

Over the past few weeks I attended a number of programmatic industry events where attendees heard about newer topics, including ad blocking and header bidding, as well as maturing topics such as viewability, transparency and tech taxes.

But it was the rising chatter about walled gardens that caught my attention and got me thinking about walled garden cycles. Unlike current topics, which will likely get resolved over the short term, walled gardens are cyclical with profound long-term implications.

The idea behind my analysis is to put advertising history under the lens of cyclical analysis in order to better understand the buy-side implications. I looked at four eras of walled gardens, in terms of bargaining power and the two main forces driving growth. It not only became apparent that innovation and investment ebb and flow from one era to the next, but also sheds light on how advertisers with data prowess will maintain bargaining power in a walled garden world.

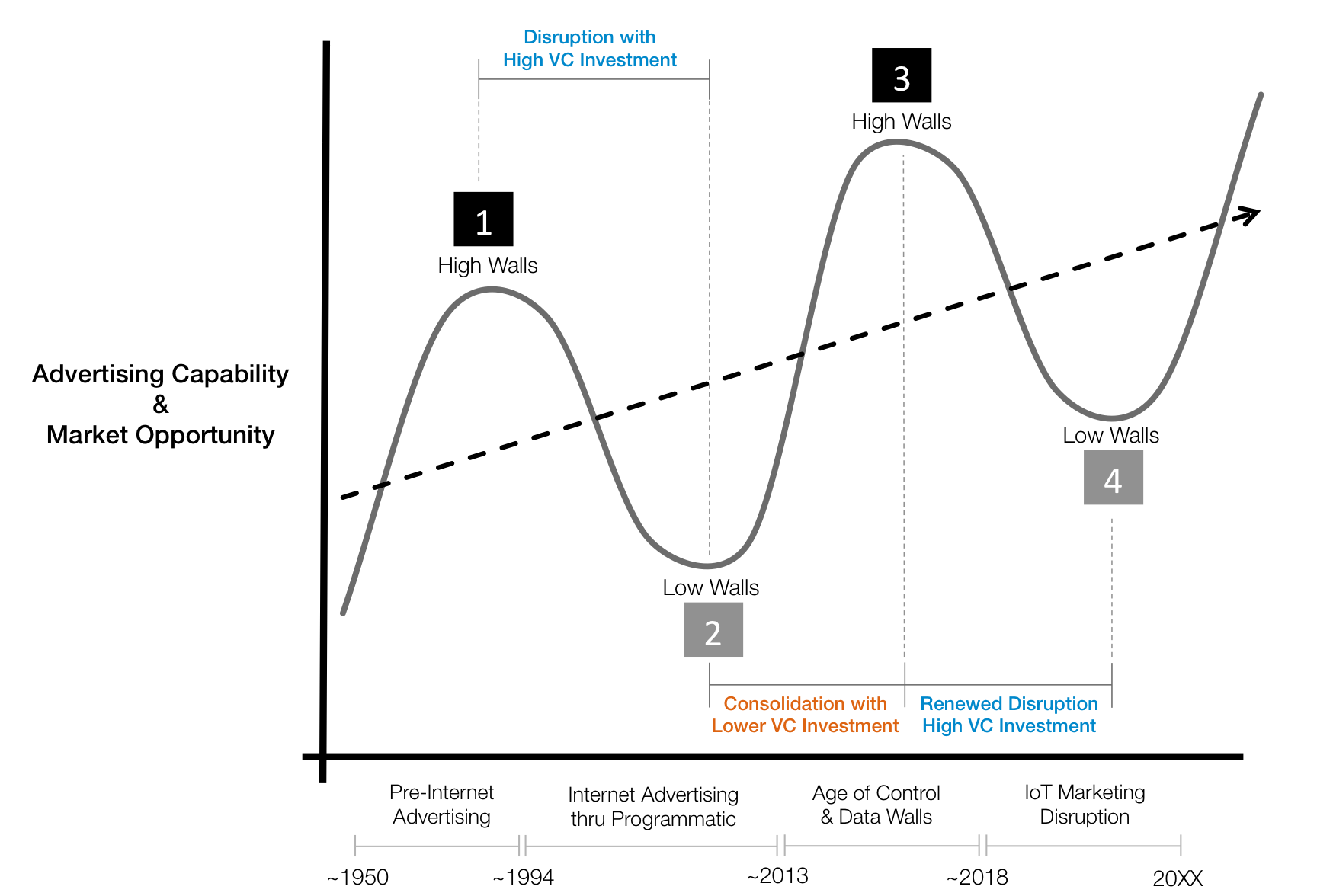

Walled Garden Era and Trends

Source: Tom Triscari. Download PDF version here.

The concept of a cycle is usually defined as the period between two consecutive peaks or troughs. The period between trough and peak is known as an expansion phase while the period between peak and trough is known as a contraction phase.

I call the vertical axis “advertiser capability and market opportunity.” Although the trend line can represent many factors, both ad tech capabilities and market opportunity seem to be the two most visible industry drivers.

For example, there is no denying the rapid growth in our industry’s ability to source, create and take action on an exponential amount of data in ever more complex ways across buying, selling and dynamic creative technologies. Moreover, ad industry revenues continue to grow in tandem with our abilities, as observed by the steady expansion of digital, programmatic and global advertising in general. Going forward, we should expect continuous growth of both drivers independent of how and when walled gardens rise and fall.

The First Two Eras Of Walled Gardens

The horizontal axis calls out four eras using rough observational time intervals of the past and best guesses going forward.

The first era to note is the pre-Internet era ranging from 1950 (probably even earlier) to around 1994, when the first display ad was served. In this era of Mad Men, there was a limited genre of supply sources, audience data was often spotty and marketers manually bought inventory directly from the content owners. The sell side had an effective walled garden bargaining advantage.

Then something amazing happened. A new utility was born. The Internet grabbed our time, attention and imagination. It created massive opportunity for tech savvy startups and cash-rich venture capitalists to forever change the way advertising was conceived, bought and executed. The Internet advertising through programmatic era shifted bargaining power to the the buy side in a big way. Not only did the walled gardens of yesteryear fall, they came tumbling down at an unanticipated pace leaving a new breed of players in control while the rest played catch up, lingered or died.

From The Crumbled Old Walls Begin Higher Walls Anew

Today we are seeing the resurrection of new walled gardens in which the bricks of better data make for a mightier wall of control. We have entered the age of control and data walls.

While many opinions at conferences and in the press put a fearful slant on walled gardens, there is actually nothing to fear. They say the Google-Facebook-Apple oligopoly is going to take over the ad world. However, what’s much more realistic is a programmatic marketplace of many walled gardens in a game of coopetition where bargaining power is constantly at stake.

For example, Snapchat, Yahoo, AOL-Verizon, LinkedIn and Amazon are all swimming in the similar directions. Then there is Comcast/NBC, CBS, GroupM/Xaxis, VivaKi OS/Sapient, Oracle, Salesforce, Adobe, all the big consulting houses and many others creating, contemplating or aiding walled garden strategies from build, buy and partner perspectives. Walled gardens are the new norm.

The Next Era?

Ad tech disruption was fueled by big VC investment during the last peak and trough phase. Now the market is experiencing consolidation, patient M&A and low investment. Going forward, we should expect to see renewed disruption and VC interest as the walled gardens of today crack open the next cycle of opportunity in the era of IoT marketing disruption.

Investment timing is everything. It separates gains from losses. This is why successful investors make bets on where the puck is going, not on where it is today. A bit of investing luck is always nice, but luck is mostly about thoughtful Goldilocks timing: Investors don’t want to be too early (overzealous optimism) and they don’t want to be too late (herd mentality). They want to time cycles just right. Investors want to feel the light at the end of the tunnel and remove all risk of it being an oncoming train. This is exactly why we look at the past to predict the future.

He Who Has The Gold (Data) Makes The Rules (Control)

All walls eventually come down. But for the foreseeable future, walled gardens are likely to grow higher and we will likely see more of them erected in 2016 and beyond. The resulting advertiser complication happens when buy-side data goes behind the wall but doesn’t come back out. How will advertisers maintain bargaining power in such a scenario and how will publishers monetize moated audiences without rich buy-side data embedded into the trade? Quid pro quo.

There will be winners and losers in this new dynamic, but only privileged advertisers with data prowess will maintain bargaining power strength. Getting there will not be easy. The winners will have very disciplined data science, always-on measurement, relentless hypotheses testing, applied game theory and totally new incentive structures. They will possess the currency that dictates the rules of the game.

What is your bargaining power plan today?

Follow Tom Triscari (@triscari) and AdExchanger (@adexchanger) on Twitter.