“Data-Driven Thinking” is written by members of the media community and contains fresh ideas on the digital revolution in media.

“Data-Driven Thinking” is written by members of the media community and contains fresh ideas on the digital revolution in media.

Today’s column is written by Ramsey McGrory, chief revenue officer at Mediaocean.

“Willy Wonka and the Chocolate Factory” is one of the greatest movies of all time. I love the movie because Willy Wonka, like me, is a paranoid optimist.

His grand utopian vision comes to life in the scene where Willy sings “Pure Imagination.” But he sweats the small stuff, literally Puma soccer shoes and an old coat, stirred in as secret ingredients for Everlasting Gobstoppers.

When I talk to leaders in media, including brands, publishers, broadcasters and technologists, I feel like we’re all paranoid optimists – or should be. When you visualize what a buyer’s (or seller’s) world will be like in 20 years, like me, you may imagine a Star Trek glass-top control panel or 3-D VR environment with displays showing paid, owned and earned media, measures of brand health, marketing campaigns in action with metrics on cross-device user exposure, engagement metrics on real sites and indicators of likely sales impact on considered purchases. Oh, and CMOs with longer tenure than 18 months.

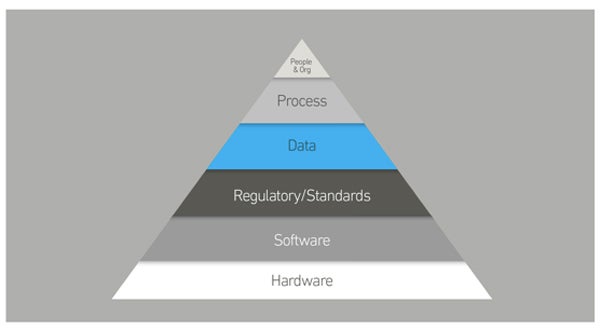

What keeps us from getting there quickly is the scale of the transformation happening. To help understand the scope and type of change happening, it’s helpful to visualize a media hierarchy of needs. (Thanks, Maslow.)

Each layer is critical to the efficient media market and efficient companies within media. And in each layer, there is transformational change happening.

Hardware: We’ve seen a massive transformation from mainframes to client servers and now the cloud. This may be the only layer of the hierarchy where we, as a media industry, all agree and understand there are a finite set of providers: Amazon, Google, IBM, Microsoft and a few others, depending on whether you’re looking for cloud storage, security or gateway infrastructure and applications.

The hardware transformation has changed from “It’s critical that I own my hardware on which my business is built” to “It’s a commodity, cheaper and more powerful when someone else provides the network on which my business is built.” In the last four years, Amazon Web Services pricing has decreased by a factor of 10.

Software: For decades in the US media and advertising market, five large buyers and a dozen large sellers bought and sold most television advertising. The software used consolidated to several providers and the costs compressed to sub-3%. Now, there are many ways to engage users.

Buyers and sellers are saddled with ad-delivery point solutions as the number of devices, supply, data, intermediaries and potential bad actors explode. An average brand’s cross-media campaign may require 10 to 15 technology, data and service providers with their own software, where costs are five to 10 times the costs of traditional with many more risks to address.

Standards and regulation: Governmental regulations such as COPPA are expanding to the pending EU privacy legislation known as GDPR. There are also self-governing digital industry guidelines on privacy, but many separate organizations with specific interests, little enforcement authority and some coordination of efforts. Brands, agencies and sellers have voiced concerns.

Data: Data has exploded in volume, variety, velocity and veracity. Nielsen was and is still the data and currency on which billions of dollars of media are transacted – but the world is changing.

Agencies will begin to use comScore/Rentrak data for 2018 planning, buying and measurement in the upfront and spot TV markets. Measurement is fragmenting from a monolithic Nielsen world to a fragmented world because there is more to measure and the sources of data are owned by many. Programmatic TV is also scaling where Nielsen and comScore are used, as well as first- and third-party data from buyers and sellers alike.

People and organizations: Nowhere is the amount of change up and down the hierarchy more evident than here. All are tied closely together and evolving to address the new realities of higher-speed, cross-channel, data-driven advertising and multichannel content distribution across owned sites and social media. Some organizations are aggressively transforming, while others are flailing under the weight of changes in consumer behavior, technology, software and data.

Rather than transforming from within, some agencies have started new organizations, such as Xaxis or Hearts & Science, to transform. Others are transforming with “front-door” strategies, pitching clients at the holding company level and pulling resources from across different operating agencies. By and large, agencies have been more agile than both advertisers and publishers in transforming.

We have a long way to go to get to a measurable, safe, predictable, integrated and automated cross-media world. It’s not happening fast enough, and we need to invest more in addressing each layer.

As Willy Wonka said, “Invention, my dear friends, is 93% perspiration, 6% electricity, 4% evaporation and 2% butterscotch ripple.”

Follow Ramsey McGrory (@NYCMcG), Mediaocean (@TeamMediaocean) and AdExchanger (@adexchanger) on Twitter.