For a long time, dynamic take rates were something ad exchanges experimented with quietly. That is changing.

Google has been doing it for years under the “Average Revenue Share” banner, and Index Exchange published its own model, positioning it as a feature. Others are moving in the same direction, some publicly and some not.

Once two major players start promoting dynamic take rates as an advantage, the rest of the field inevitably gets pulled in. The alternative is losing share to whoever moved first.

The pitch for dynamic take rates is reasonable. Instead of charging a fixed commission on every impression, the exchange takes a larger cut on high bids and a smaller one on low bids. The average take rate stays roughly the same. Total volume goes up. The exchange shows growth, the publisher sees more impressions clearing, and everyone moves on to the next thing.

The problem shows up when you think about where the extra volume comes from.

Moving money around

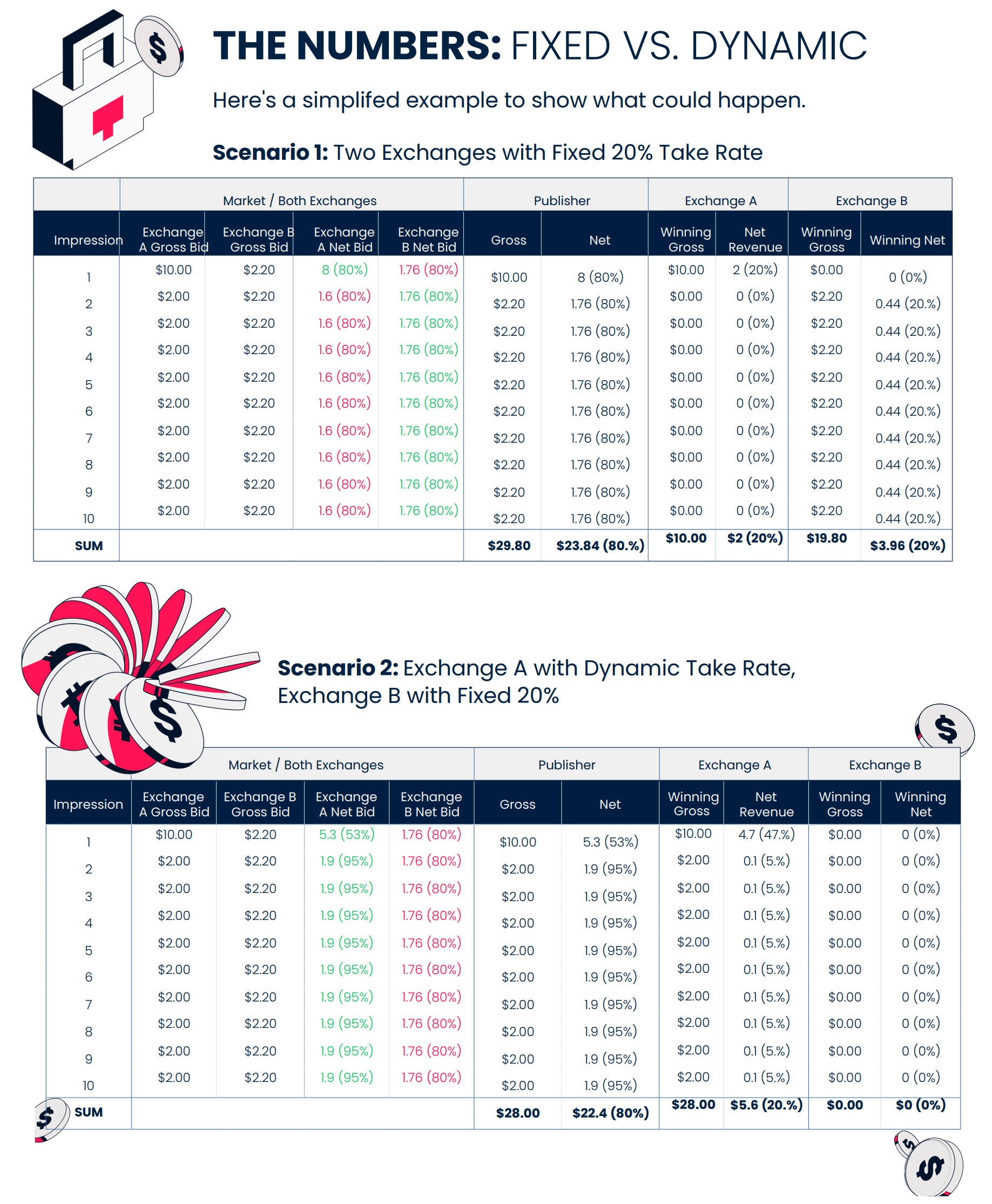

Historically, if an exchange sees a $10 bid on a given impression, it would normally keep 20% of that bid. Under dynamic take rates, it keeps more, using that extra margin to top up nine other bids that would have otherwise lost.

The exchange still comes out at a 20% blended rate, but it has now won impressions it could not have won at a fixed rate. On the exchange’s own dashboard, the win rate is up, revenue is up, and publisher volume is up.

But here is the part that doesn’t show up in the dashboard: Those nine subsidized impressions were not sitting unsold. Another exchange, or another buyer, would have cleared them. The publisher was already going to earn something on that inventory.

When the first exchange “pays the publisher back” by winning those extra impressions at slightly higher prices, that’s not new revenue; it’s replacing revenue the publisher would have earned anyway from other buyers. The publisher essentially lent real dollars (from the high bid) and was repaid in inventory that already had value. The return on that loan is far less than what was lent.

Take 10 impressions with specific CPMs and walk through how many cents the publisher lent versus how many were returned when the SSP has a fixed take rate vs. a dynamic take rate.

In scenario 2 above, the publisher ended up netting roughly 6% less revenue when one exchange had dynamic take rates in effect.

Who’s losing out

The math proves who pays for the subsidy. The advertiser on the high bid is the one financing the rest of the bids. That money does not go to the seller they intended to buy from, and it does not stay with the publisher either. It goes to underwriting cheaper inventory being bought by different advertisers on a different demand-side platform.

Premium demand ends up subsidizing performance demand, and the DSPs that specialize in brand spend lose the most because they are paying the tax. The DSPs that specialize in low CPMs also lose because the pool of inventory they can actually afford keeps shrinking as the subsidized bids crowd them out.

None of this requires anyone to act in bad faith. A fixed-rate exchange in a dynamic-rate market loses bids, then loses share, then gets deprioritized through supply-path optimization. They eventually get routed around entirely. It is a textbook prisoner’s dilemma, and the exchanges caught in it did not design the game.

If the game’s structure is what drives adoption, the fix cannot come from the sell side. No sell-side platform is going to volunteer to cede market share to a competitor that has already moved.

The only parties capable of changing the incentive are the ones writing the checks on the high end: the holding companies, the agencies and the DSPs representing premium brands. They are also the ones losing the most money to the subsidy, whether they know it or not.

Every exchange should be able to answer a direct question about how its commission varies from bid to bid. Log what they say, and let that inform supply-path decisions.

This isn’t a boycott or a naming-and-shaming campaign; it’s baseline price discovery. Transparency on take rate behavior should not be a radical request.

I’m expecting this problem to get worse over time. Once dynamic take rates are the norm, every exchange will be running optimization on two variables at once: how much margin to borrow from high bids and how efficiently to spend it on subsidies. The better everyone gets at both, the more value leaks out of the system. Whatever the drag is today, it will be larger next year.

I would rather see the industry deal with this while it involves a few players. Once dynamic take rates are universal, unwinding them will be a different problem entirely.

“The Sell Sider” is a column written by the sell side of the digital media community.

Follow Primis and AdExchanger on LinkedIn.

For more articles featuring Rotem Shaul, click here.