“On TV And Video” is a column exploring opportunities and challenges in advanced TV and video.

“On TV And Video” is a column exploring opportunities and challenges in advanced TV and video.

Today’s column is written by Tyler Pietz, principal at Two Rock Consulting.

In wake of a recent series of highly publicized ad tech scandals, a gaggle of leading industry figures has wondered aloud if brands might be better served by withholding their digital ad dollars from the likes of Google and Facebook and going back to basics with direct deals with TV networks and other well-known, premium video publishers. At this year’s upfronts, TV executives doubled down on this narrative.

However, even if one is to accept this prescription prima facie, it belies a more insidious reality: With linear television viewership already in decline, networks are strategizing as to how they can wiggle out of legacy rate agreements to match demand with an accelerated wane in supply.

That leaves digital, and given the option, consumers are rejecting premium ad-supported video content en masse for subscription-based ad-free options. The leading providers of premium, digitally distributed content will become increasingly willing to oblige them.

That last statement may come as a controversial prognostication. The conventional wisdom from industry folks seems to be that it is only a matter of time before giants such as Netflix and Amazon cede to the siren call of ad revenues, or that ad-supported rivals will appear from the ether and provide marketers with the captive eyeballs and wallets that TV once did.

However, the available evidence would seem to support the contrarian wisdom that the multichannel model is under direct siege from the Netflixes and Amazons of the world, which have woven healthy, ad-free business models seemingly out of whole cloth.

The Hulu Case

Hulu is something of an anomaly among pure-play digital video providers. As opposed to linear MVPDs, which rely on a combination of subscription and ad revenue, on-demand digital video distributors are typically bifurcated into free, ad-supported full-episode players or subscription-based services that do not show ads.

Hulu falls somewhere in between the two. A sort-of joint venture between the major US television networks, it started life as a free-to-watch full-episode player business supported by advertising. It eventually introduced an $8-per-month subscription service called Hulu Plus, which provided unfettered access to its content library, greater device availability – the free tier is desktop-only – and a reduced ad load.

Roughly a year and a half ago, Hulu shook up its subscription business by introducing an ad-free offering at $12 per month alongside its free tier and Hulu Plus tier, which contains roughly half the ad load of the free tier.

This doesn’t necessarily suggest – intrinsically, at least – that the incremental value of serving ads to a single user is just $4 per month. One possible explanation could be that there is a tiny subset of users who reject ads outright, and that by adding a less profitable ad-free tier, Hulu can grow its overall subscriber base without cannibalizing a more profitable “plus” tier.

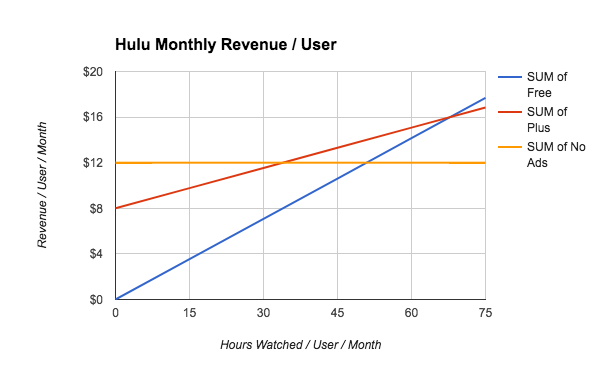

In digging into the microeconomics, however, it becomes abundantly clear that video ads are not the astronomically lucrative revenue stream they are often made out to be. Consider the below data table and chat, in which I’ve estimated Hulu’s revenue per user, per month, given some basic assumptions:

| Estimated avg. CPM of 30-second video ads | $22 | ||

| Selling, general and administrative expenses (SG&A), at 33% of sales | $7.26 | ||

| Revenue per ad view | $0.015 | ||

| Sub-tier | Free | Plus | No Ads |

| Price | $0 | $8 | $12 |

| Est. ad load / hour (30-second ads) | 16 | 8 | 0 |

| Est. ad revenue / hour | $0.24 | $0.12 | 0 |

| Est. ad views to break even | 814 | 271 | 0 |

| Est. content hours to break even | 51 | 34 | 0 |

Even before factoring in the (massive) fixed costs associated with operating an ad sales division, and given a charitable estimate for SG&A and average CPM of 33% and $22, respectively, the meager penny or two that a company such as Hulu earns on each individual ad view equates to roughly 34 hours per month of viewed content hours before it can close the $4 revenue gap between its plus and no-ads tiers:

This begs a serious question: How many users who are willing to pay $8 per month for a premium subscription service will balk at the prospect of an additional $4 per month in exchange for watching ads, which interrupt their content experience? And how many free users can it realistically expect to sit in front of a laptop screen for more than 50 hours each month to reach the $12 per month in revenue it would command from a premium subscriber?

Other Considerations

Beyond the linear returns demonstrated on the above chart, there are two additional factors at play that challenge the ad-sales model on which video content distributors have typically relied.

First, the very presence of ads has been shown to have a negative impact on viewership time. It’s difficult to quantify the exact causal impact of this phenomenon, but Hulu itself has acknowledged this implicitly in the past, and plenty of macro-level data suggests this.

Namely, Netflix, which is ad-free, commands roughly 1.5 times the monthly time spent from its users than does Hulu – 30 hours vs. 60 hours, by some estimates – despite the enviable recency, breadth and depth of Hulu’s content library, which led Netflix CEO Reed Hastings to describe Hulu as a “cord-cutter’s dream.”

It also makes intuitive sense: It’s ridiculous to imagine that anyone would prefer to have their content interrupted with ads, particularly in a non-live setting.

Second, there is a quickly diminishing economic return in showing the same ad to the same user – most advertisers endeavor to frequency cap for this very reason. A single person or household will only spend so much on shaving products or carbonated beverages, meaning that unique reach is paramount in ad effectiveness.

There is much to infer from shifting content consumption patterns and the resulting economics, which suggest the future of premium, scripted video content will be increasingly devoid of ads. Netflix and Amazon continue to increase their expenditures on premium, long-form content and provide it to the end user in a more cost-effective, user-focused and ad-free fashion than their legacy competitors, and this will continue to make those legacy models less advantageous.

Long-sought improvements in relevance (audience targeting) and user experience (fewer, less interruptive ads) are ideals of which every ad-driven business should take heed, but the end may already be nigh for ad-supported premium, on-demand video.

Follow Tyler Pietz (@tylerpietz) and AdExchanger (@adexchanger) on Twitter.